Quantum computing is an emerging field promising to solve problems so complex that even the world's most powerful supercomputers would need longer than the age of the universe to crack them. Rigetti Computing (RGTI +19.94%) sits at the center of this exciting narrative.

For a brief window, investors treated the company like the next great artificial intelligence (AI) play. But shortly after the stock became a phenomenon, reality arrived. With shares now down 66% from all-time highs, here is what smart investors should understand before touching Rigetti stock.

Image source: Getty Images.

What does Rigetti Computing do, and why should investors care?

At its core, Rigetti builds superconducting quantum processors. These chips harness the principles of quantum mechanics to perform sophisticated calculations that classical computing systems fundamentally cannot.

The company sells access to its quantum systems through a cloud-based infrastructure and also makes physical hardware for government agencies and research institutions. Rigetti stock went parabolic in late 2024 and throughout 2025 -- riding a sector-wide frenzy ignited by Alphabet's unveiling of its Willow quantum chip.

As one of the few publicly traded pure-play quantum names, Rigetti became a vehicle for speculative investors who wanted exposure to the next AI mega-theme.

Rigetti's financial results illustrate a harsh reality

Rigetti's financial results are difficult to defend under any conventional valuation framework. In 2025, the company generated approximately $7.1 million in revenue -- a modest decline from the prior year. Meanwhile, net losses exceeded $216 million on a generally accepted accounting principles (GAAP) basis.

During the first quarter of 2026, the company showed signs of sequential improvement, with revenue of $4.4 million. However, operating losses for the quarter persisted.

Rigetti's price-to-sales (P/S) multiple of 607 is not a rounding error. It signifies an expectation that the company will one day generate revenue commensurate with an enterprise valued at $6.2 billion. Unfortunately, there is no near-term evidence supporting this outlook.

Rigetti is a falling knife, not a dip to pounce on

There are other concerns with Rigetti beyond the company's headline losses. First, insider selling has been a consistent theme. This time last year, Rigetti CEO Subodh Kulkarni sold roughly 1 million shares near the stock's peak for approximately $11 million -- a move that could suggest the frothy valuation is disconnected from underlying fundamentals.

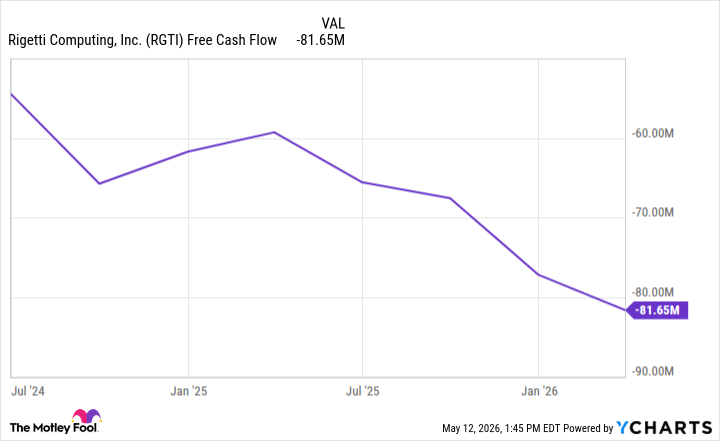

Second, the company's operating losses are structural, not transitory. Rigetti is burning through capital at nearly $100 million per year. The silver lining is a liquidity position approaching $570 million with no meaningful debt on the balance sheet. While this buys Rigetti several years of runway, this does little to validate the company's already-struggling business model.

RGTI Free Cash Flow data by YCharts

The gap between the enthusiastic narrative around quantum computing and Rigetti's actual numbers remains wide. Revenue is barely moving, losses are mounting, and insiders have been selling the stock on strong upswings.

Investors eyeing the pullback in Rigetti stock as a potential second-chance entry should be more prudent. A stock down from its high can always fall further, especially when the valuation premium remains unjustified even after the sell-off. Without a commercial breakthrough or a rapid acceleration in revenue, Rigetti looks less like a dip worth buying and more like a speculative falling knife.