Idaho housing market

The median sales price for a single family house in Idaho in July 2023 was $479,400, down 0.63% year over year. But just because sales are down doesn't mean that the real estate market is cooling in Idaho. In fact, the number of homes for sale is also down significantly -- over 30% from July 2022, with just three months of supply available to any given buyer.

Climbing mortgage rates aren't deterring buyers, 13.8% of single family homes sold in July 2023 were sold above list price and overall, the market still is holding fast to pricing, with the average home selling for 98.4% of its list price during this period

Idaho also has low property taxes. These average 0.69% of a home's assessed value. For a home worth $479,400, that's about $3,308 a year in property taxes.

How do I calculate my mortgage payment?

Idaho mortgage rates are higher than they have been in years, so it's important to compare rates from the best mortgage lenders . Our helpful mortgage calculator will help you determine your mortgage payment in Idaho.

For example, if you're taking out a 30-year fixed $400,000 mortgage at 7.5%, our Idaho mortgage calculator shows that you'll be looking at a monthly payment of $2,818.00 for principal and interest.

However, your total monthly costs will be higher, because you'll need to account for other expenses. Our Idaho mortgage calculator estimates some of these costs to give you a sense of what they might look like. These include:

You can also play around with our Idaho mortgage calculator and determine your monthly costs based on different loan or down payment amounts.

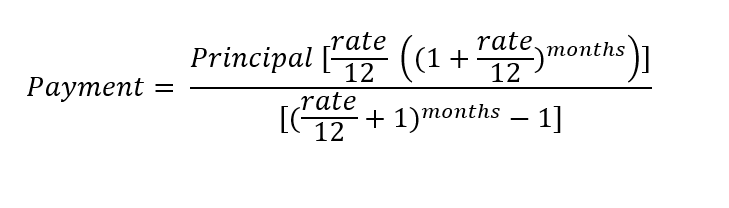

If you want to calculate your monthly payment without the help of the mortgage calculator, you can use this formula:

'%3E%3CanimateTransform attributeName='transform' type='rotate' repeatCount='indefinite' dur='2s' values='0 364 104;360 364 104' keyTimes='0;1'/%3E%3C/circle%3E%3C/svg%3E)

Things to know before buying a house in Idaho

As a general rule, your mortgage payment inclusive of property taxes, homeowners insurance, PMI, and HOA fees should not exceed 30% of your gross income. For example, if your household's combined gross income is $9,000, you'll be limited to $2,700 for your inclusive mortgage payment. Use our Idaho mortgage calculator to find out what you'll pay

Of course, there are other expenses you'll need to budget for, too. Maintenance and repairs are irregular (but necessary) expenses of homeownership. Keep in mind that our Idaho mortgage calculator doesn't include maintenance or repairs in its numbers -- you'll need to factor those in on your own.

Maintenance

You'll need to account for maintenance, which could cost anywhere from 1% to 4% of your home's value per year. It's hard to know what end of that range your costs will fall into. A lot depends on the age and condition of your home, its size, and the size of your yard and property. You'll find a lot of the money you'll spend on maintenance will relate to exterior items, like lawn care and landscaping. A good way to know what you're in for is to pay attention during your home inspection. The inspection will reveal a lot about the condition of your home.

Repairs

You'll also need to factor home repairs into your budget. Those can be a lot less predictable than maintenance. You can allocate $100 a month for repairs, but if a $2,500 boiler fix creeps up on you, that $100 won't cut it. If you make a point to save that $100 during those months when you don't end up having repairs, you'll have an easier time covering costly fixes when they do pop up.

Build a solid emergency fund -- one with enough money to cover three to six months of living expenses -- before buying your home. That will give you a way to pay for repairs without going into debt.

Tips for first-time home buyers in Idaho

The Idaho Housing and Finance Association has a number of programs designed to help first-time home buyers.

Depending on your income and credit score, you may qualify for these options:

- Fannie Mae or Freddie Mac HFA Preferred loans, which allow down payments of as little as 3% for first-time buyers

- The First Loan FHA/VA/RD program, which offers reduced-rate mortgages to those who qualify for a FHA, USDA, or VA loan

- Forgivable loans for down payments and closing costs

- Second mortgages for down payments and closing costs, which allow for a loan of up to 3.5% of a home's sale price or appraisal value

- A Mortgage Credit Certificate, which gives buyers a tax credit of up to $2,000 annually for mortgage interest paid each year

You should also know there are steps you can take as a first-time buyer to increase your chances of getting approved for a mortgage in Idaho, and at a competitive rate. These include:

The more effort you make in these regards, the smoother the mortgage application process is likely to be.

It's also worthwhile to research the differences between adjustable- and fixed-rate mortgages. You might be impressed by the low rates offered with adjustable-rate mortgages, but you should know all the details involved before signing up for one. Fixed-rate mortgages may have slightly higher interest rates, but the payments will be more predictable.

Are you ready for a mortgage in Idaho?

If you're ready to buy a home in Idaho, use our Idaho mortgage calculator to see what your monthly home loan costs will be. But also, don't just accept the first mortgage offer you get. Rather, reach out to different mortgage lenders for quotes.

Each lender sets its own rates and criteria, so you may find that your mortgage costs are less expensive with one lender than another. In fact, once you get your lowest offer, you can plug it into our Idaho mortgage calculator and see how much you're saving by shopping around.

Still have questions?

Here are some other questions we've answered: