If you've heard that becoming an S corporation could save you boatloads on self-employment taxes, you're not alone. The promise of lower tax bills has catapulted S corporations to the top of the list among tax structures for small businesses.

Lawyers and tax experts are less enthused. One tax attorney wrote in The National Law Review that S corporations are "rarely advisable" and the tax savings are "often illusory."

Another attorney wrote for the American Bar Association:

"There is practically nothing that can be done by or with a corporation that cannot also be done equally well or better with an LLC."

Why the mismatch? Can an S corp save you money over a limited liability company (LLC) or not? Let's compare and find out.

What is the legal classification of an LLC?

An LLC is a legal business entity formed by filing articles of organization with your secretary of state. Its owners are called members.

LLCs were independently created by state statutes and are governed by the laws of their home states.

What is the legal classification of an S corporation?

An S corporation is a federal tax status, not a legal business entity. To become an S corporation, you must form a legal entity, such as a traditional corporation or an LLC.

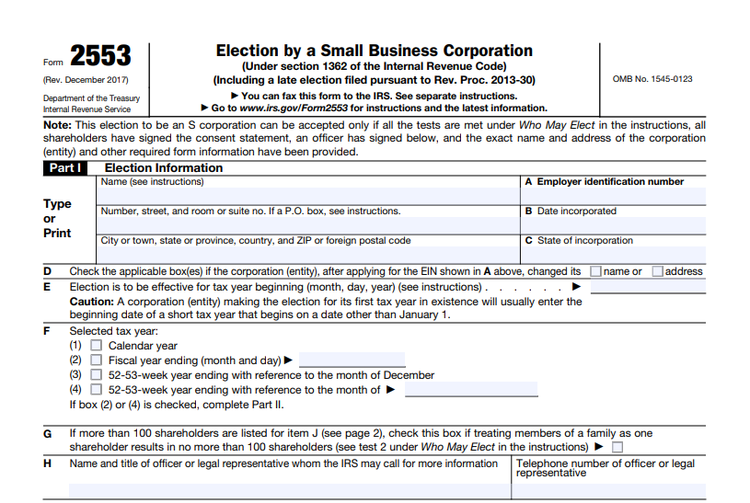

Then you must elect S corporation status by timely filing Form 2553, Election by a Small Business Corporation, with the Internal Revenue Service (IRS).

Existing LLCs wishing to elect S corporation status must file Form 8832, Entity Classification Election, before filing Form 2553. Businesses must meet strict eligibility requirements for S corporation status.

For multi-member LLCs, this usually requires revising the company's operating agreement to align with the requirements.

While S corporations aren't legal entities, they impose new rules on businesses electing them. That's why they can be so hazardous to unsuspecting entrepreneurs.

'%3E%3CanimateTransform attributeName='transform' type='rotate' repeatCount='indefinite' dur='2s' values='0 375 251;360 375 251' keyTimes='0;1'/%3E%3C/circle%3E%3C/svg%3E)

Eligible businesses can elect S corporation status by filing IRS Form 2553. Image source: Author

S corp vs. LLC: How taxes are treated

Both S corporations and LLCs are pass-through entities, which means profits pass directly from the business to the owners as personal income. This eliminates the double taxation levied on traditional corporations.

All profits from an LLC must be passed through to its members each year. The profits don't have to be distributed, but they must be allocated and taxed.

The company doesn’t file an LLC tax return. Instead of an LLC tax, the members report profits as income on their personal tax returns and pay federal income tax and self-employment tax on them.

S corporations provide more options. Owners of an S corporation, called shareholders, can pay themselves a reasonable salary for their work, withhold payroll taxes, and pay the employer's share of payroll taxes as a business expense.

They can then take additional profits as distributions from the business, which are tax-free until they exceed the owners' stock basis in the company. Stock basis, or equity basis, is basically an owner's investment in a company calculated according to the tax rules that apply to the entity.

The bottom line is that S corporation distributions are not subject to self-employment taxes and may even be tax-free, resulting in a low S corp tax rate.

Owners of S corporations have flexibility in how much they want to reinvest in the company and how much they want to draw as income. However, distributions must be taken in proportion to the shares held by each owner. This eliminates the LLC's flexibility in divvying up profits.

As pass-through entities, both LLCs and S corporations are eligible for the qualified business income (QBI) deduction. For S corporations, the deduction would apply to income taken as distributions, not salaries.

Taxes for an S corp vs. taxes for an LLC

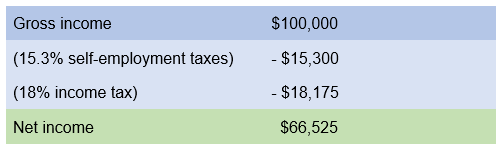

A florist does business as a single-member LLC. The business makes $100,000 in profits after expenses. The owner would report the profits as personal income on Schedule C of IRS Form 1040. The owner's federal taxes might break down like this:

'%3E%3CanimateTransform attributeName='transform' type='rotate' repeatCount='indefinite' dur='2s' values='0 252 76;360 252 76' keyTimes='0;1'/%3E%3C/circle%3E%3C/svg%3E)

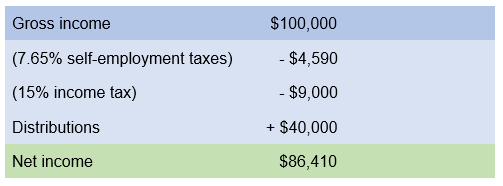

If the florist formed an S corporation, the owner could draw a salary of $60,000 from the business and take $40,000 as a distribution. Now the federal tax picture is:

'%3E%3CanimateTransform attributeName='transform' type='rotate' repeatCount='indefinite' dur='2s' values='0 251 93;360 251 93' keyTimes='0;1'/%3E%3C/circle%3E%3C/svg%3E)

Note that the business would still be paying the employer's share of payroll taxes, so there is no employment tax advantage on the share of income taken as salary.

The big difference is in the distributions. If the florist's stock basis is more than $40,000, those distributions could be tax-free. So why not just pay yourself a starvation salary and take the bulk of your profits home in distributions?

First, the IRS requires that owners draw a reasonable salary based on common-sense benchmarks such as comparable salaries in your area. Setting your salary unreasonably low for tax purposes can prompt the IRS to rescind your S corporation status.

Second, the tax situation for your business could be very different. It takes an accountant, or ideally, a tax attorney to determine the implications of the S corporation structure for your business.

In addition to federal tax nuances, some states tax S corporations differently, so you need to look at state and federal taxes before drawing any conclusions.

Should you form an S corp or an LLC?

LLCs and S corporations have unique advantages and drawbacks.

5 benefits of an S corp

- Pass-through taxation: As pass-through entities, S corporations are not subject to corporate income tax.

- Tax savings: Distributions taken beyond salaries are not subject to self-employment taxes and may be tax-free.

- QBI deduction on distributions: An S corporation can let high-income earners who would otherwise be phased out capture more of the QBI deduction.

- Access to investment capital: S corporations may have up to 100 shareholders, allowing the business to attract investment capital.

- Limited liability: Shareholder liability is limited to the amount invested in the business.

7 disadvantages of an S corp

- Shareholder restrictions: Shares must be held only by U.S. citizens or residents, so LLCs, corporations, and other entities can't invest in the S corporation.

- Stock restrictions: You may issue only one class of stock, which means that distributions must be made in strict proportion to shares of ownership.

- Limited losses and deductions: Shareholders cannot claim losses and deductions beyond their stock basis.

- Regulatory complexity: S corporations must meet more complicated and stringent regulatory requirements, requiring additional documentation and professional advice to maintain. Taxes returns are also complex.

- Added costs: S corporations generally cost more to form and maintain than LLCs.

- Legal hazards: Many businesses inadvertently violate S corporation shareholder and stock restrictions. When that happens, they may revert to corporate tax status.

- Challenges of dissolution: If S corporation status doesn't work out for you, you can't simply switch back. Shareholders must vote to dissolve the corporation, which may trigger significant taxes. The IRS also requires businesses to wait five years before changing tax elections.

'%3E%3CanimateTransform attributeName='transform' type='rotate' repeatCount='indefinite' dur='2s' values='0 375 244;360 375 244' keyTimes='0;1'/%3E%3C/circle%3E%3C/svg%3E)

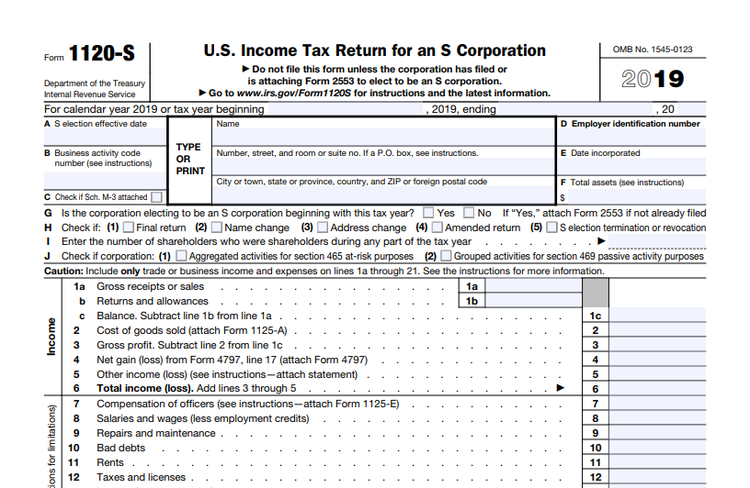

S corporations have a lot more paperwork to manage than LLCs, including corporate tax returns Image source: Author

.

Source: IRS.gov.

7 benefits of an LLC

- Pass-through taxation: Because profits pass through to the members' personal income, LLCs are not subject to corporate income tax.

- QBI deduction: All income from an LLC is eligible for the QBI deduction.

- Flexible profit sharing: LLC members can split up profits as they wish, according to the terms of their operating agreements.

- Simplicity: LLCs are relatively simple to create and maintain, with far less paperwork to manage than an S corporation. Since profits pass through to personal income, taxes are simple, too.

- Limited liability: LLC members are shielded from personal liability for business debts and lawsuits.

- Low costs: Because of their simplicity, starting an LLC costs less, and the savings continue year after year.

- Active management and control: LLC owners retain broad, flexible powers to manage and control the business.

3 disadvantages of an LLC

- Self-employment tax: All income from an LLC is subject to self-employment tax.

- Annual profit allocation: All profits from the business must be allocated to members and taxed each year.

- Limited duration: Generally, if a member leaves your LLC, the entity must be dissolved and a new one created.

And the winner is...

The S corporation structure might make sense for a business that has only one or two owners and generates far more in profits than what the owners would earn as salaries. Even for those businesses, though, the benefits may be negligible given that the self-employment tax phases out as your income increases.

While the S corporation election may be a good move for some businesses, it's not a do-it-yourself project. If you're tempted by the tax benefits of an S corp, consult with an expert first.