Artificial intelligence (AI) stocks were hot in recent years, but that began to change in 2026. Wall Street's "Great Rotation" away from the technology sector this year resulted in plunging share prices. The tech-heavy Nasdaq Composite was particularly affected, entering correction territory in the first quarter.

The shift in sentiment was caused by a number of concerns, including massive capital expenditures by the likes of Microsoft (MSFT +4.15%). But according to Morningstar, "This AI stock currently looks 38% undervalued relative to our $600 fair value estimate."

Indeed, Morningstar's view that Microsoft is undervalued rings true. Here are the factors that make the tech veteran a compelling growth stock to buy now and hold for the long term.

Image source: Getty Images.

Microsoft's capex costs make sense

Microsoft shares sank over 10% this year through April 21, and hit a 52-week low of $356.28 on March 30. Wall Street punished the tech giant for capital expenditures (capex) of $37.5 billion in its fiscal second quarter ended Dec. 31, which was a jaw-dropping 66% year-over-year increase.

Concerns over that enormous capex jump are understandable, especially since ChatGPT creator OpenAI accounts for 45% of Microsoft's remaining performance obligations (RPO). The dependence on one customer for such a significant amount of RPO is a valid worry, but as a leader in artificial intelligence, OpenAI is growing at an unprecedented pace. It was generating $1 billion per quarter at the end of 2024, and now that's up to $2 billion per month.

The once-in-a-generation opportunity presented by AI justifies Microsoft's capex. In the race to be an AI leader, the company is in an enviable position. To remain there, it needs to build up its infrastructure.

The company is the world's second-largest cloud computing provider behind Amazon. However, its cloud infrastructure was assembled using tech that's no longer sufficient for the advanced capabilities required of AI systems, necessitating the capex spending to perform required upgrades.

NASDAQ: MSFT

Key Data Points

Why Microsoft stock is a buy

The infrastructure investment is already paying off. Microsoft's fiscal Q2 revenue rose 17% year over year to $81.3 billion as its cloud division sales grew 29% to $32.9 billion. Its gross margin also increased 16% year over year, contributing to net income jumping 60% to $38.5 billion.

These results are excellent and likely to strengthen, since the AI sector is still in growth mode. Industry forecasts project the AI market will reach $335 billion this year, climbing to $1.3 trillion by 2032, providing Microsoft with a tailwind for years.

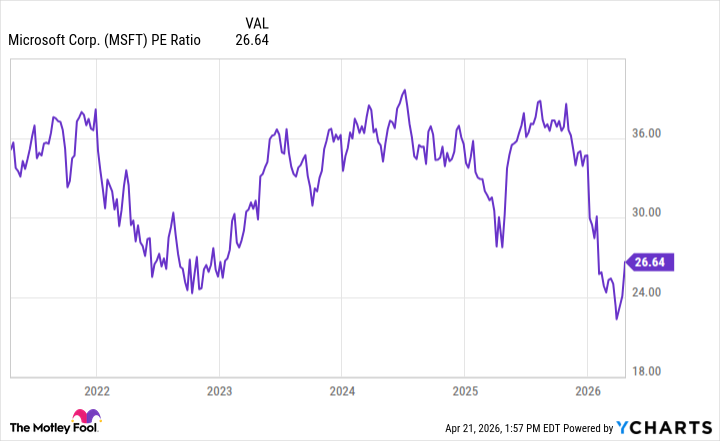

Given the company's business performance, Wall Street's reaction to its capex spending looks overblown, considering the tech titan's share price valuation plunged to a multiyear low. This is evident in its price-to-earnings ratio.

Data by YCharts.

As the chart shows, investors are starting to recognize Microsoft is undervalued, causing its earnings multiple to edge upward of late. However, it's still below where it's been for the past couple of years, so the opportunity to pick up shares at an attractive valuation remains.