SpaceX's IPO valuation relies pretty heavily on the company's artificial intelligence (AI) business. Here, Musk and team are renting a Memphis data center to Anthropic and Alphabet's (NASDAQ:GOOG) Google for about $26 billion a year combined. That's incredible. But when you read the fine print, you learn that either company can cancel the contract with 90 days' notice.

Furthermore, the AI business operates in a competitive space and is burning through cash faster than the rockets and Starlink businesses can make it. Overall, SpaceX lost $4.28 billion in a single quarter and $41.3 billion since its founding.

That shouldn't be too concerning, given Musk's success at turning Tesla (NASDAQ:TSLA) into a financial juggernaut. (Tesla has net savings of $37 billion on its balance sheet, and it generated over $6 billion in free cash flow last year).

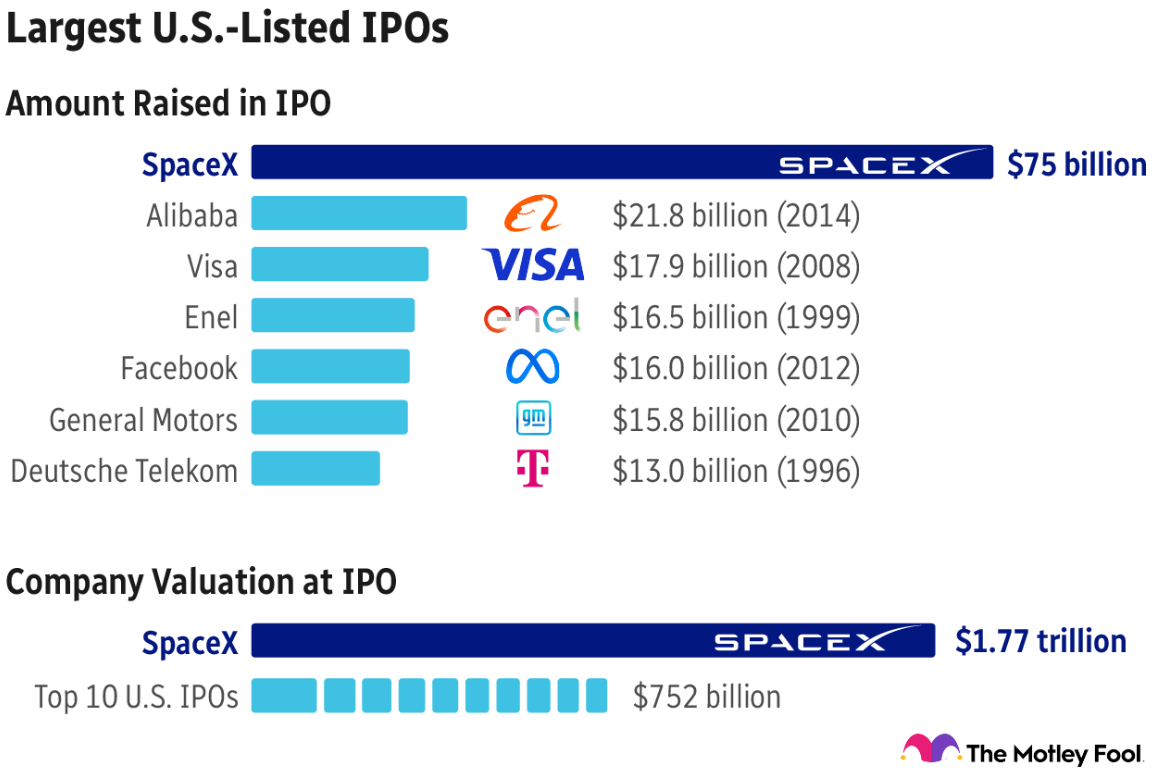

The trouble is that, at SpaceX's opening valuation, investors will be paying 95x sales. When you pay 95x sales, you're not buying today's performance. No, you're discounting years of uninterrupted excellence. You're betting that nearly everything goes right, quarter after quarter, for many years.

In a market already above the 90th percentile of historical valuation, stacking that much unbridled optimism on top of SpaceX feels like the wrong move to us.