The recent surge in stocks tied to artificial intelligence (AI) offers some tempting but uncertain opportunities to investors. Without a doubt, many of these stocks have made huge returns in short amounts of time. Still, to buy most of those stocks now requires paying a high valuation, which exposes you to the risks of a slump should the AI story come to an abrupt pause or halt.

If investors still want to invest in AI stocks under such conditions, they should probably look for companies with low stock valuations -- ones that have not attracted as much attention as the most popular names.

Today, I'm focused on one such under-the-radar stock that could deliver significant long-term return: cybersecurity company SentinelOne (S +7.61%). As of the time of this writing, a $3,000 investment would buy about 192 shares.

Image source: Getty Images.

The under-the-radar stock

Cybersecurity is a highly competitive industry, and companies such as CrowdStrike and Palo Alto Networks seem to capture much of the attention.

Moreover, investors recently turned more doubtful on the entire business model's outlook as Anthropic's AI engine, Claude, exposed numerous vulnerabilities within many cybersecurity platforms. That finding has led to questions about whether AI could disrupt the industry.

However, with that in mind, IT professionals want a platform that will stop these threats, which could specifically benefit SentinelOne. It stands out because it built its Singularity platform from the ground up around AI.

With that, it has evolved from an endpoint protection tool to a comprehensive security platform centered on agentic AI, known as Purple AI. Since SentinelOne decentralized Purple AI to the point that it can address threats at the endpoint, it is different from the cloud-centered (and centralized) systems that may not respond as quickly or effectively to cyberattacks.

Other benefits include behavioral AI detection to quickly find anomalies within a system. Also, with Singularity Cloud Security, AI-powered detection combined with automated responses can protect workloads, virtual machines, and containers.

SentinelOne by the numbers

Additionally, despite all the doubts about cybersecurity companies, clients have not stopped turning to SentinelOne. In its fiscal 2026, which ended Jan. 31, its revenue rose 22% to $1 billion.

That revenue gain did not prevent it from posting a quarterly loss of $451 million in an environment where Palo Alto and CrowdStrike earned profits. Still, much of that negative result was driven by its $298 million in stock-based compensation expenses.

Its free cash flow was positive, and improved to almost $52 million in fiscal 2026 versus less than $7 million in the prior year.

This leaves the company in a solid fiscal position. Although it had issued shares to raise cash, the positive free cash flows reduced that need. Moreover, it is debt-free and has $629 million in liquidity that it could either invest in itself or deploy to acquire other companies that could expand its competitive advantages.

NYSE: S

Key Data Points

SentinelOne stock also holds potential for gains because investors do not seem to appreciate the company's positioning. The stock is about 80% below the all-time high it set in 2021, and has largely traded in a range since 2023. That may make the stock look like one to avoid, considering that Palo Alto and CrowdStrike trended higher over much of that period.

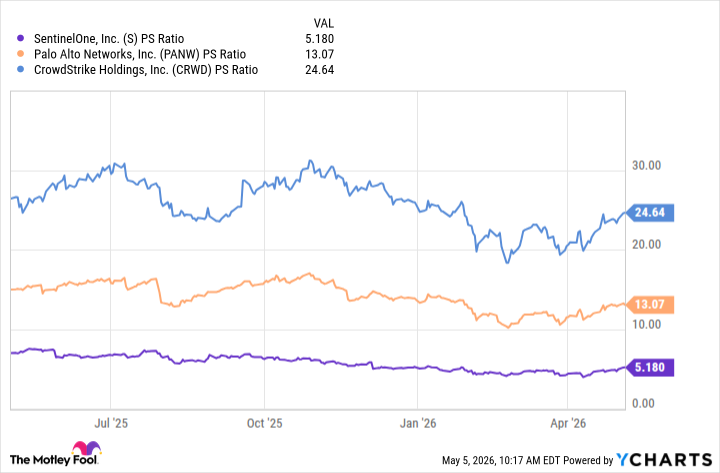

Still, that also means it trades at a price-to-sales (P/S) ratio of 5, far cheaper than Palo Alto Networks or CrowdStrike.

S PS Ratio data by YCharts.

Also, SentinelOne's market cap is $5 billion, making it a fraction of the size of Palo Alto and CrowdStrike, which have market caps of $149 billion and $119 billion, respectively. That lower entry point could give SentinelOne investors considerable room for gains.

Buying SentinelOne stock

If you have $3,000 to invest in an AI company now, it may pay to take a chance on SentinelOne.

Admittedly, the stock has stagnated even as rivals like Palo Alto and CrowdStrike have risen, and its ongoing net losses in an environment where larger rivals earn profits may bode poorly on the surface.

Fortunately, the recent narrative about AI's potential to kill software stocks is likely wrong. Moreover, SentinelOne has the advantage of operating a platform built around AI from the beginning. That could better position it to address threats increasingly powered by that technology. Additionally, its positive free cash flow mitigates the effects of its bottom-line losses and positions it to continue innovating, which may strengthen competitive advantages over time.

Finally, since its revenue continues to grow and its 5 P/S ratio likely limits the stock's further downside risk, investing $3,000 in SentinelOne could turn out to be a profitable move over time.