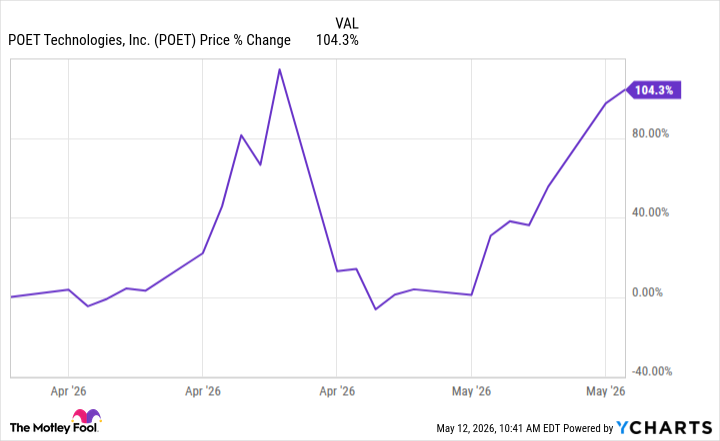

There's a new player emerging in the world of artificial intelligence (AI) infrastructure. Over the last month, shares of Poet Technologies (POET 22.36%) have surged by more than 100% amid heavy trading volume and speculation about the company's future role in AI data centers.

Is Poet poised to become the next big winner in AI infrastructure, or is this yet another hype-fueled meme narrative destined for a sharp reversal?

What is photonics, and why is it important for AI development?

Modern AI server clusters are packed with hundreds of thousands of GPUs. When training and powering huge models, these architectures generate enormous volumes of data that must move among chips, servers, and racks within milliseconds.

Data movement accounts for a large portion of energy consumption in AI systems. And as data transfer speeds climb, the standard copper interconnects between the various components and servers become strained.

Photonics aims to sidestep these problems. Instead of transmitting data along copper wires using electricity, the technology does it by sending pulses of light through optical waveguides and fiber optic cables -- a method that delivers dramatically lower power consumption. In theory, this process can support higher bandwidth density and reduce thermal demands. This also enables tighter rack packing -- a subtle cost advantage as hyperscalers accelerate their AI build-outs.

Poet's Optical Interposer integrates both photonic and electronic components directly onto a single silicon wafer.

Image source: Getty Images.

Poet stock has garnered huge enthusiasm, but smart investors should be skeptical

The recent surge in Poet's share price reflects excitement about the company's supposed technological edge in its niche. Retail traders and momentum investors have bought into the narrative that it's an under-the-radar player poised to disrupt the multitrillion-dollar AI infrastructure market.

The reality is that it is tiny by revenue standards. In 2025, the company generated roughly $1.1 million in sales. Operating losses exceeded $30 million, driven by heavy spending on research and development. With these figures in mind, it appears that meaningful product revenue and profitability are still years away for Poet.

With a market capitalization hovering around $2 billion, Poet's current valuation profile implies enormous expectations. A price-to-sales ratio (P/S) of 949 is a premium of a magnitude that is rarely justified. Unless the company starts rapidly capturing a meaningful slice of the optical interconnect market, dilution from future capital raises or declines due to execution missteps will likely erode shareholder value.

Parabolic potential with the risk of cratering shares

Could Poet stock go parabolic? The addressable market for data center equipment should continue expanding as next-generation applications come online, with big tech focusing more on inference-focused deployments.

A first-mover advantage in wafer-scale photonics could compound in value rapidly as developers integrate more optical equipment into their data centers. If Poet begins converting AI tailwinds into recurring revenue by landing production orders with major developers, then the stock could easily become a multibagger.

NASDAQ: POET

Key Data Points

What's more likely, however, is continued high volatility, and there's a legitimate risk that the share price will crater. Without top-line acceleration and a demonstrated path to profitability, Poet's lofty valuation leaves little margin for error. Any delays in customer adoption, issues achieving manufacturing scale, or emerging competitive responses could also trigger a sharp sell-off.

Poet's price action historically has featured numerous explosive gains, which were often followed by abrupt pullbacks. These dynamics already illustrate how sentiment can pivot based on headlines rather than concrete fundamentals. The stock's extreme swings, microscopic revenue base, and dependence on future execution make it an unsuitable holding for most people's portfolios.

High-risk speculators might allocate a small, actively managed position to Poet in a bid to capture some upside from macro AI infrastructure themes. But for most investors seeking durable wealth creation, Poet should be watched from the sidelines.