Nebius Group (NBIS 1.08%) stock has set the market on fire over the past year, rising 5.3x in such a short time. The incredible hunger for artificial intelligence (AI) data center computing capacity has been a tailwind for Nebius' business, which explains the parabolic jump in its stock price.

Nebius is a neocloud company that builds dedicated AI data centers and rents out computing capacity to customers. It also offers software development and management tools that allow customers to build, deploy, scale, and fine-tune AI applications. So, Nebius is more than just a landlord renting out AI data center compute.

It is a full-stack infrastructure provider that aims to offer end-to-end solutions for customers looking to develop and deploy AI applications and enhance productivity. Not surprisingly, Nebius' business model is proving to be hugely successful, and investors have been buying this AI stock hand over fist, given its solid long-term growth potential.

Let's look at the reasons why Nebius could make you substantially richer over the next three years.

Image source: The Motley Fool.

Nebius' business model should ensure terrific long-term growth

Nebius is filling a key gap in the AI infrastructure ecosystem by building new data centers. Additionally, its software-focused offerings should ensure that customers renting compute capacity continue to spend more money with the company. Nebius' software stack allows customers to run inference tasks, build agentic AI applications, train models, and fine-tune models as per their requirements.

NASDAQ: NBIS

Key Data Points

Customers purchasing tokens to run software-centric applications should ideally boost Nebius' margins and earnings over the long run. The good news is that the company's full-stack AI infrastructure strategy is reaping fruit. Its revenue in the first quarter of 2026 jumped by 7.8x year over year to $399 million. More importantly, Nebius' adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) jumped to $129.5 million last quarter from a loss of $53.7 million in the year-ago period.

Nebius' adjusted EBITDA margin stood at 32% last quarter. The company believes that it is on track to end 2026 with an adjusted EBITDA margin of 40%. What's more, Nebius' growth is poised to accelerate as the year progresses. The company's annualized run rate revenue is expected to go up from $1.9 billion in Q1 to a range of $7 billion to $9 billion by the end of 2026.

Nebius anticipates overall revenue to land between $3 billion and $3.4 billion this year, a potential jump of 6x from last year's revenue at the midpoint. This phenomenal growth in Nebius' top line is supported by the company's aggressive data center build-out. Nebius was operating 170 megawatts (MW) of active data center power capacity at the end of 2025. The company is targeting 800 MW to 1 gigawatt (GW) of connected capacity by the end of this year.

This aggressive capacity expansion will enable Nebius to convert the lucrative contracts it has with Meta Platforms and Microsoft into revenue. Nebius noted on the latest earnings call that it will begin delivering cloud computing capacity to these Magnificent Seven companies in the third and fourth quarters of 2026.

More importantly, Nebius is shoring up its long-term data center pipeline, which should ensure that its red-hot growth continues beyond 2026. It now expects to close 2026 with 4 GW of contracted data center power capacity, up significantly from the 3 GW forecast it issued in May. The contracted power capacity refers to the agreements Nebius enters into with power and utility companies to secure the electricity needed to set up additional data centers.

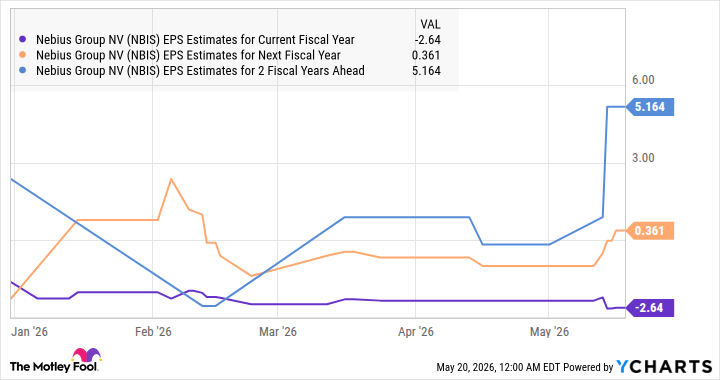

Nebius, therefore, seems well-positioned to achieve its long-term target of deploying 5 GW of active data center capacity by the end of 2030, which will be around 5x the active capacity it expects this year. The additional infrastructure that Nebius will bring online should also help it sell more software services. This probably explains why analysts have become more bullish about the company's bottom-line growth prospects.

Data by YCharts

The stock could more than triple in just three years, and here's the math behind it

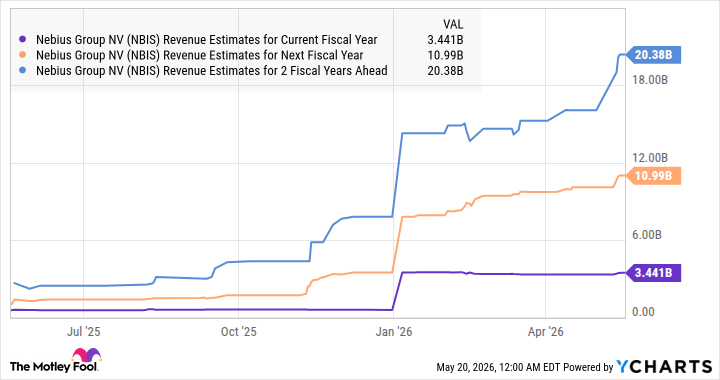

Nebius' contracts with Meta and Microsoft put its potential revenue backlog at over $46 billion. That's a huge number, given the revenue it is expected to generate this year. I have already pointed out that the aggressive build-out of Nebius' data centers will help it quickly convert that sizable backlog into revenue. So, it is easy to see why analysts are anticipating a substantial surge in its top line through 2028.

Data by YCharts

Nebius, of course, could do better than that by winning new contracts and accelerating its data center build-out. But even if it manages to achieve $20.4 billion in revenue in 2028 and trades at just 8 times sales after three years (a slight premium to the U.S. tech sector's average sales multiple of 7.5), its market cap will reach $163 billion.

That's 3.2x Nebius' current market cap, suggesting this growth stock could easily trade above $600 within the next three years. So, it isn't too late for investors to buy this high-flying stock following the remarkable gains it has clocked over the past year.