Having confidence in a stock can mean multiple things. However, when I say I've never been more confident in a specific stock than I am right now, I am combining market-crushing returns with confidence. Those two attributes are rarely found together, as higher potential returns are normally associated with higher risk, but that doesn't seem to be the case with Nvidia (NVDA 1.00%).

Nvidia's success is tied to the data center build-out, and the hyperscalers and other leaders in this infrastructure expansion are largely approaching the trend with their cards on the table. Their public spending forecasts give investors a fairly clear idea of what will happen next, and the outlook is quite positive for Nvidia. That's the reason why it occupies the largest position in my portfolio now.

Image source: Getty Images.

Nvidia's projections are exciting

Nvidia has completely tied its business to the data center build-out. During Q1, $75.2 billion of its $81.6 billion in total revenue came from its data center division. Nvidia's OK with that level of concentration; indeed, there have been several reports that it's considering moving away from the gaming market to focus even more on its data center product lineup. Based on the growth rates that segment is delivering, it would make sense.

NASDAQ: NVDA

Key Data Points

Broadly speaking, the company expects major growth in data center capital expenditures. This year, artificial intelligence hyperscalers set a record for planned capital expenditures, with the big four hyperscalers planning capex of around $650 billion. In 2027, that figure is expected to top $1 trillion. However, 2027 is just the start. By 2030, spending is projected to range from $3 trillion to $4 trillion.

That would be a massive market expansion in just a handful of years, and investors shouldn't write this prediction off as outlandish. Nvidia has visibility into future demand that individual investors don't have. While its forecast may not prove precisely correct, I think investors need to consider the possibility that it could be mostly right. If that's the case, there's extreme upside available for Nvidia's stock.

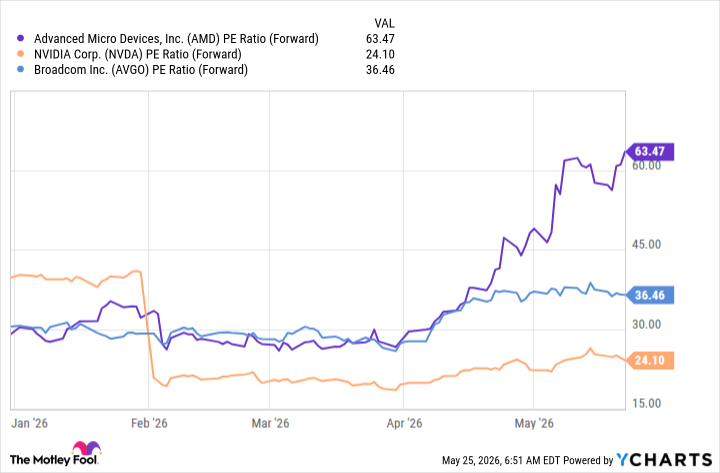

Nvidia doesn't have a premium valuation despite its growth rate

In Q1, Nvidia's revenue growth rate accelerated to 85% year over year. Top-line increases of that scale are unheard of for megacap companies, so the market really doesn't know what to do with this data. If Wall Street valued Nvidia in the same way it rates some of its peers, its stock would be 2 or 3 times its current price.

AMD PE Ratio (Forward) data by YCharts.

However, the market isn't giving Nvidia the credit it deserves. That makes it both a growth and a value stock. Whenever you can find a stock that meets both of those criteria, load up on it.

I believe Nvidia is a lock to strongly outperform the S&P 500 (^GSPC +0.22%) over the next few years. That makes it a buy in its own right. Still, if you examine the entire stock market, there are few companies with as little guaranteed growth as Nvidia, as its products have cemented themselves at the core of a multitrillion-dollar infrastructure build-out. Nvidia offers a rare combination of growth, value, and limited risk, which makes me as confident in the stock as I have ever been in any stock before.

Even if you missed out on its previous climbs, you don't need to miss out now. There's still time to buy Nvidia stock and position yourself for huge gains.