Gavin Baker, the Chief Investment Officer of the hedge fund Atreides Management, has established itself as one of the top tech investors operating today.

In eight years managing the OTC Portfolio at Fidelity, Baker achieved a compound annual return rate of more than 19% and outperformed 99% of his peers on Morningstar.

At Atreides, Baker now oversees around $7 billion in public and private investments, and, though his complete returns aren't public, he does have a Sharpe ratio of 2.46, according to Tipranks, well above the average hedge fund, meaning he's able to achieve higher returns without taking on more risk.

Baker also shares his insights on social media, and he just dropped a gem on AI stock valuations.

Speaking on the All-In podcast, he described the AI sector as "cross-sectionally inefficient," explaining that the multiples in the sector don't make sense relative to one another.

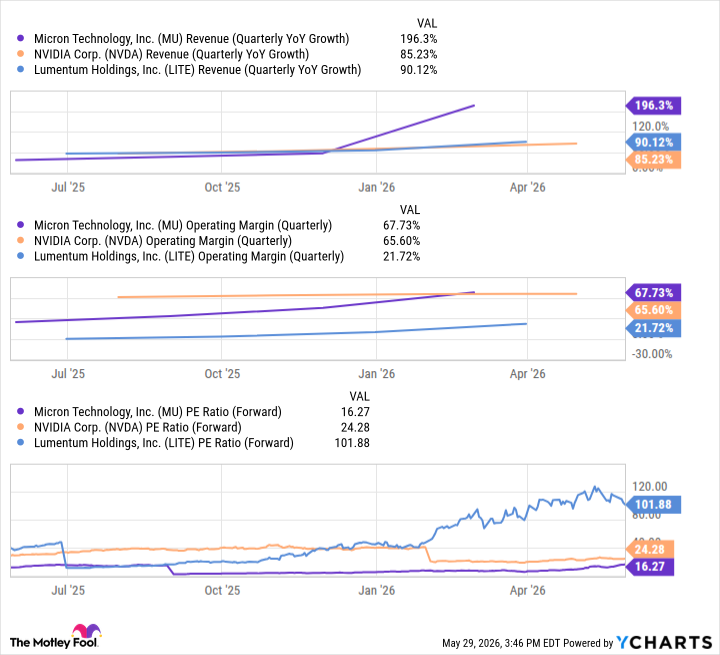

As he observes, memory stocks like Micron (MU +5.07%) and Sandisk (SNDK +3.25%) are cheap right now. Baker also says Nvidia (NVDA 1.00%) is trading at a really low P/E.

Conversely, he said that multiples in stocks dealing with power, cooling, and optical are much higher. Stocks like Lumentum Holdings (NASDAQ: LITE), an optical chipmaker that has jumped 10x over the last year, trade at a triple-digit price-to-earnings ratio. Similarly, Coherent (COHR 4.11%), another optical stock that has soared over the last year, trades at a triple-digit P/E.

Baker goes on to conclude that if the multiples on stocks like Coherent and Lumemtum are correct, then memory and Nvidia stocks should go a lot higher. On the other hand, if multiples on Nvidia and Micron are correct, then those other stocks are likely to underperform.

Image source: Getty Images.

Is there just one AI cycle?

Baker's theory assumes that there is one AI cycle driving all of these stocks. According to the line of reasoning above, the optical names are in the same AI cycle as memory stocks like Micron. If the AI boom continues, they'll win, but if it fades, they'll be losers.

Memory chip stocks have a history of cyclicality, and investors are wary of another boom-and-bust in the sector as prices can fluctuate wildly due to shifts in inventory from gluts to shortages.

Cyclicality is prevalent across the semiconductor sector, including in optical chips, though the cycles have historically been more severe in memory. What is different about AI is that it has sent these stocks off the charts, arguably making history less useful by comparison, as some have argued AI is a secular boom. If supply/demand dynamics change, however, the downside of the cycle could be brutal.

The smart way to invest in AI stocks

While momentum can trump valuation in the short term, valuation almost always matters eventually, so the cheaper stocks do have the advantage here. As the chart below shows, Lumentum stock is significantly more expensive than Micron and Nvidia, even though it's not growing faster, and it's much less profitable on a margin basis.

MU Revenue (Quarterly YoY Growth) data by YCharts

Part of Lumentum's gains over the last year have come from multiple expansion, while that isn't true of Micron, and Nvidia's valuation has actually fallen.

Following Baker's commentary, it looks like the smart way to invest in AI stocks is to choose cheaper names like Micron and Nvidia and avoid stocks like Lumentum that have relied on multiple expansion for growth.

If the AI sector rises and falls as a whole, the cheaper stocks should outperform the pricier ones over the long haul.