Intel (INTC 11.92%) made a bold move in 2021, establishing Intel Foundry to manufacture chips for third-party customers. Success didn't come right away, and Intel ultimately ousted the CEO who put the company on this path.

Nearly a year ago, Intel stock began taking off after the U.S. government announced plans to convert grants and other funding into an $8.9 billion equity investment to support a domestic semiconductor supply chain. Such strong government support comes with instant credibility. Since then, some very high-profile tech companies have shown interest in Intel's foundry services, and the stock is up a whopping 453% in just the past 12 months.

Intel's story isn't over, but here's why investors who have enjoyed the ride might want to take some profits.

Image source: The Motley Fool.

The onus is now on Intel to deliver

Reports emerged in April that Intel was in discussions with Amazon and Alphabet to provide advanced chip packaging services for their custom artificial intelligence (AI) processors. Then, in May, Intel and Apple reportedly struck a preliminary deal for producing some of the chips used in Apple's devices. These companies are whales in the technology space, so any deals struck with them would be a potential game changer for Intel Foundry.

But discussions and preliminary agreements are a far way from sealed, signed purchase orders. The stock's rally has begun pricing in success that technically hasn't happened yet, which means there's increasingly more room for the stock to fall than continue higher. In the first quarter of 2026, Intel Foundry posted an operating loss of $2.4 billion on $5.4 billion in revenue. It must continue to grow before it's a positive contributor to Intel's broader business.

Beyond simply landing deals, it must prove that it can deliver to its customers. Taiwan Semiconductor Manufacturing is the industry leader in part because it excels at producing high-end chips at the highest production yields.

NASDAQ: INTC

Key Data Points

There's far less upside than before, while risks remain

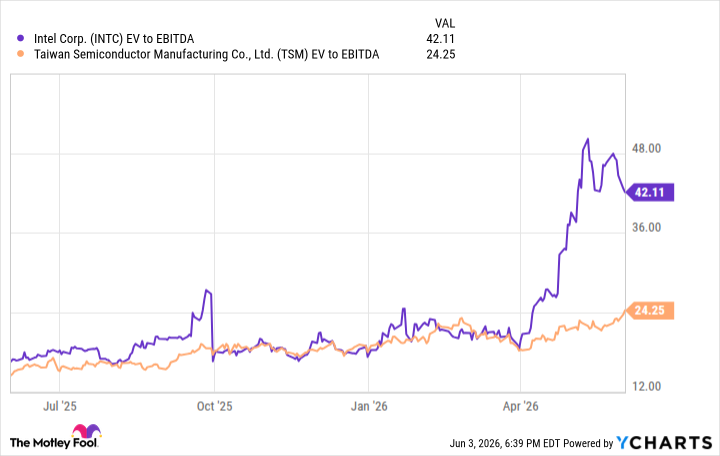

The stock's furious rally has shot Intel's enterprise value up to $568 billion, 42 times its EBITDA (earnings before interest, taxes, depreciation, and amortization). That's far above TSMC's ratio of 24. It's really hard to see how Intel can realistically justify such a premium to the bona fide industry leader, especially considering that Intel still has much to prove.

Data by YCharts. EV = Enterprise value. EBITDA = Earnings before interest, taxes, depreciation, and amortization.

And while the government's backing can help Intel, the tricky thing about political tailwinds is that they can stop blowing in your favor. The midterm elections are coming later this year, and then another Presidential election in 2028. The political landscape may change over the next two to three years, and it might not be for the better.

Add it all up, and Intel's magnificent run is a fantastic opportunity to lock in a profit and take some money off the table. It's fair to keep some Intel shares if you want to wait this story out, but at the very least, there's far less upside in the stock now than there was even a few months ago.