Nvidia still dominates the market for chips used in artificial intelligence (AI) data centers. But AI is such a tremendous opportunity that second place isn't so bad in this case. Statista estimates that the AI chip market will continue to grow, reaching $333 billion by the end of the decade.

That leaves plenty of room for other companies to make investors quite a bit of money over the coming years. Broadcom (AVGO 7.49%) and Advanced Micro Devices (AMD 11.01%) would be two prime candidates. Both have made inroads with their AI chips, but when it's all said and done, one stands out above the other. Here's why Broadcom is likely the better AI chip stock to own.

Image source: Getty Images.

AMD is picking the harder fight

The million-dollar question is, how does a smaller company compete with the industry giant? Advanced Micro Devices, or AMD for short, is primarily competing head-to-head with Nvidia in general-purpose AI chips. To its credit, AMD has gotten some traction; data center revenue grew by 57% year over year to $5.8 billion in the first quarter of 2026.

NASDAQ: AMD

Key Data Points

AMD is naturally going to see some opportunities from the AI hyperscalers who don't want to put all their eggs in Nvidia's basket. AMD recently announced plans to supply Meta Platforms with 6 gigawatts of its Instinct GPUs, including a custom version for the first gigawatt. But it's unlikely that AMD will ever threaten Nvidia's stranglehold, since Meta and other Nvidia customers have already leaned heavily on Nvidia's CUDA software.

Broadcom's custom silicon road map makes it the winner

To make a dent in Nvidia's moat, you need to take a new path. Broadcom has done just that with its XPU chips. Instead of emphasizing general-purpose AI chips, Broadcom is co-designing custom chips for each customer's AI workloads. That creates efficiency gains and can also build a stickier relationship with that customer. Broadcom is working with Anthropic, Alphabet, Meta Platforms, and OpenAI, among others, on custom silicon. It is a big opportunity as compute shifts from training to inference, where efficiency matters more.

NASDAQ: AVGO

Key Data Points

Wall Street sold off Broadcom hard for its second-quarter earnings, mainly because its third-quarter AI revenue guidance came in below expectations. However, CEO Hock Tan reiterated the company's long-term expectation of $100 billion in annual AI chip sales starting in fiscal year 2027. Broadcom generated $10.8 billion in AI revenue in the second quarter, so there's still significant growth ahead as these custom silicon projects roll out.

Broadcom is worth the premium

Given Broadcom's list of high-profile AI customers and continued momentum toward $100 billion in annual AI chip revenue, it's hard not to like Broadcom's competitive position more than AMD's at this point. Investors may notice that Broadcom stock is more expensive than AMD's, but the premium seems justified.

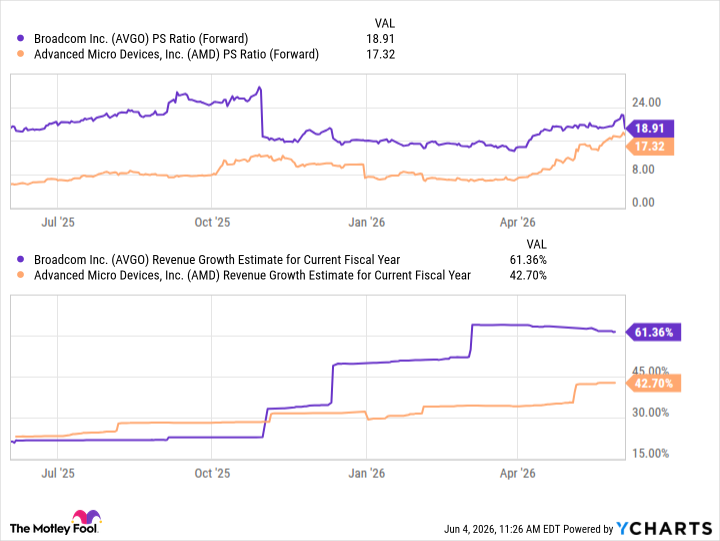

AVGO PS Ratio (Forward) data by YCharts

Analysts see far faster growth ahead for Broadcom compared to AMD, and the valuation gap between the two isn't that wide. Broadcom is where you want to put your money, especially after this post-earnings dip.