However, this rule comes as a shock to some people because it supersedes the well-known rule that you must wait until age 59 1/2 to take retirement account withdrawals without taxes and penalties. That means, even if you're older than 59 1/2 when you withdraw, some of your withdrawal could be taxable, thanks to this five-year rule.

You won't owe the 10% penalty in that case. But you will still owe tax on any withdrawals above the amount contributed.

2. Roth conversions

There's also a separate five-year rule that applies only to those who convert other types of retirement accounts into Roth IRAs. The idea of this rule is to prevent people from using Roth conversions to get penalty-free access to their traditional retirement accounts before age 59 1/2. The rule doesn't apply if you're over that age.

This five-year rule also starts the clock on January 1 of the year you do the conversion. As a result, those who convert late in the year have to wait only a bit longer than four years before taking withdrawals.

However, this five-year rule differs in that it applies separately to each Roth conversion you make. Each new conversion starts its own five-year clock, and you'll need to account for multiple conversions to ensure you don't withdraw too much money too soon.

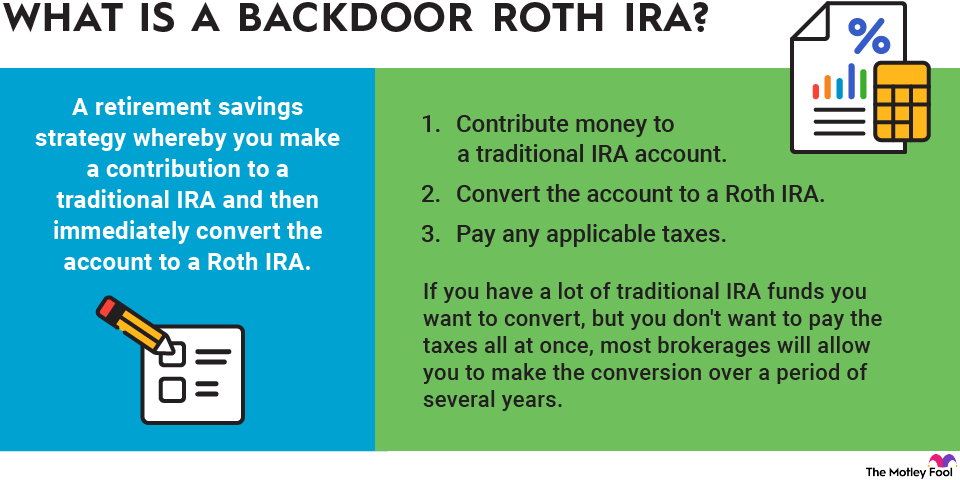

Note that the five-year rule applies equally to Roth conversions for both pretax and after-tax funds in a traditional IRA. That means if you're using the backdoor Roth IRA strategy every year, your "Roth contributions" are really conversions, and you can't withdraw them for five years without penalty.

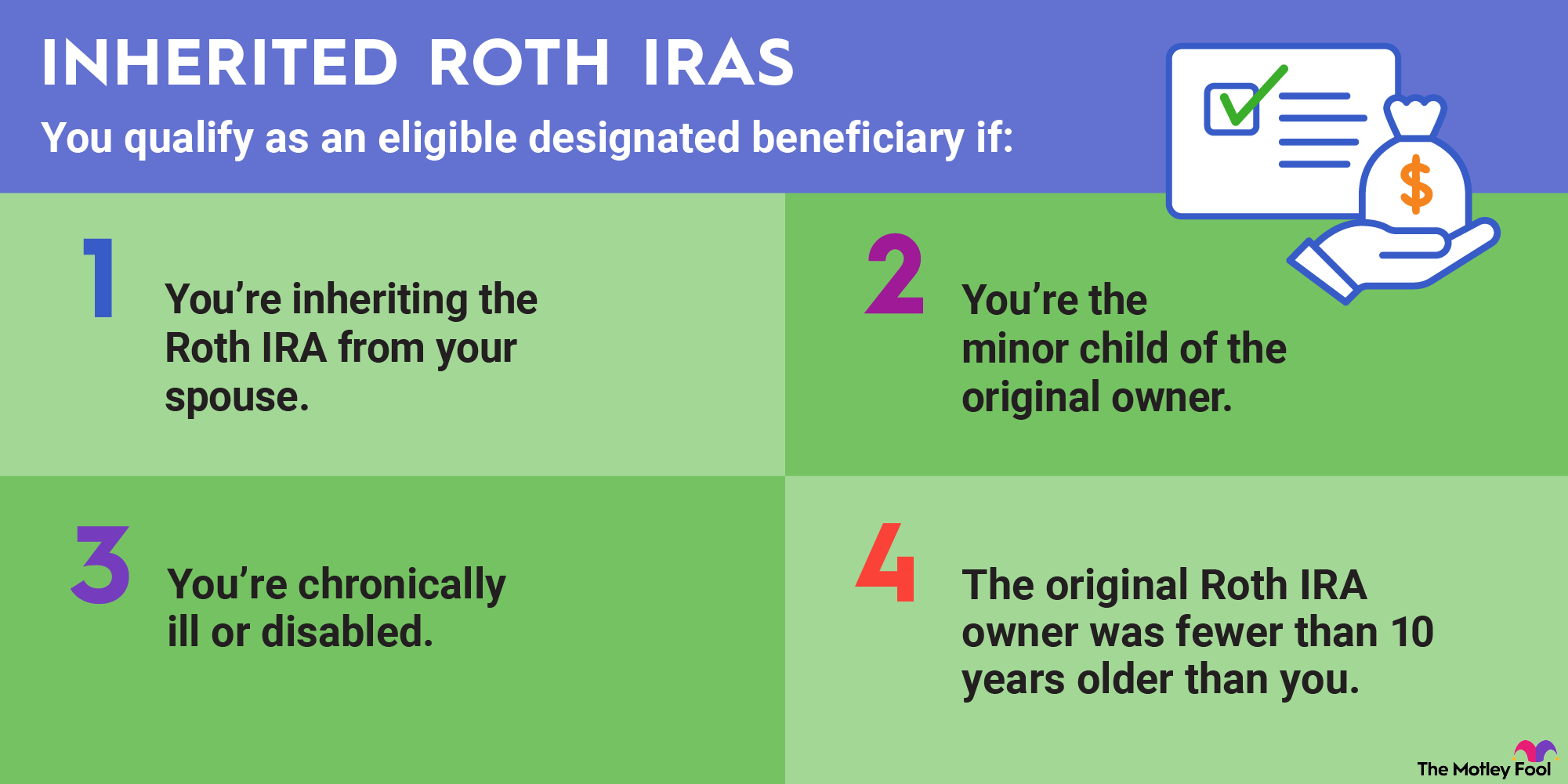

3. Inherited IRAs

If you inherit a Roth IRA from someone other than your spouse, you have a couple of options for withdrawing the funds. You have 10 years to deplete the inherited IRA, but RMDs may be necessary.

The 10-year rule applies only to Roth IRAs inherited from someone who died after 2019, per the SECURE Act rules. For Roth IRAs inherited from someone who died in 2019 or earlier, the pre-SECURE Act rules apply.

In the latter case, the 10-year rule is a five-year rule, meaning the account must be depleted by the end of the fifth year unless the beneficiary is taking annual distributions based on their life expectancy.

Inherited IRAs are also subject to the first-contribution five-year rule. Therefore, if it has been less than five years since the owner's initial contribution to a Roth IRA, the earnings are subject to taxation. Keep that in mind if you want to withdraw a lump sum early.

Penalties for breaking the five-year rule

- Your first contribution: Withdrawing funds from a Roth IRA less than five years after your first contribution requires account holders to pay taxes on the earnings portion of the withdrawals. However, Roth IRA withdrawals prioritize contributions before earnings. That means you may be able to make a tax-free withdrawal less than five years after your initial contribution if you have enough cumulative contributions to cover the amount.

- Roth conversions: If you withdraw money from a converted Roth IRA within the first five years after the conversion, you'll have to pay a 10% penalty on any withdrawals. That includes withdrawals of the amount you initially converted, even though you've already paid taxes on that amount. However, you can still use other exceptions to the 10% penalty rules in a Roth conversion situation. In particular, if you're older than 59 1/2, the age exception applies, and you can immediately take withdrawals without worrying about the penalty.

- Inherited IRAs: If you fail to withdraw 100% of the funds from an inherited IRA by the end of the fifth year following the owner's death (for IRAs inherited from someone who died in 2019 or earlier) or the 10th year (if the death occurred in 2020 or later), the remaining balance is subject to a 25% penalty. The penalty is reduced to 10% if corrected within two years.